Tuesday, 29 April, marked a proud milestone for the Indigenous Consumer Assistance Network (ICAN) as its Grow Officers officially graduated in a heartfelt ceremony at The Chambers in Cairns. The event celebrated academic achievement, cultural leadership, and financial empowerment of the next generation of First Nations financial wellbeing advocates.

The graduates, Elise, Sinead, Libby, and Fred, each brought their unique voices and experiences to the day, reflecting on the journey that led them to this moment and the powerful future they are helping to build.

“It’s a pretty special moment,” said Elise. “Graduating alongside my colleagues makes it even more meaningful, our hard work has paid off. This is for my parents and my Aunty Joyce and Uncle Peter (dec), for all the things they had to forgo raising all of us kids. I’ve also followed in the footsteps of my Aunt Susan Cook, who was one of the first First Nations financial counsellors in Australia. It’s such an honour to walk the path she helped pave.”

For many, the course provided more than just theory, it brought about real-life transformation.

“Being the youngest in the course, it opened my eyes about making big purchases in the future,” said Sinead. “It allowed me to see where people with little financial literacy go wrong, and what I can look out for to make informed decisions.”

Libby shared how the learning has extended beyond the classroom and into her home.

“It’s been great. I have been sharing my knowledge with my son, and he has achieved some awesome goals, like saving and being able to read contracts when he was purchasing his car,” she said.

Each graduate spoke of the doors opened through the ICAN Learn scholarship program – opportunities they now use to empower others in their communities.

“It’s opened the door for me to deliver financial counselling services in the local prison,” Elise explained. “That’s important to me, especially with the overrepresentation of First Nations people in custody. Many offences are money-related, so getting in there and delivering financial literacy can make a difference.”

All the graduates echoed the importance of representation in the financial wellbeing sector.

“Having more First Nations people within this sector means voices can be heard a lot more, especially when advocating on systemic issues that only a First Nations person can understand,” said Fred.

“As a First Nations person, reaching out for help and feeling shame can be a big issue,” Sinead shared. “But as a First Nations service worker, you can relate to a client’s situation and have a deeper cultural understanding. Having someone you can connect with can knock down some barriers and make engaging other First Nations people easier.”

As for what’s next, Libby’s goals reflect a powerful commitment to breaking cycles and creating futures.

“My goals for the future are to start and complete my financial counselling diploma and purchase a house so that I can create generational wealth for my children.”

And Elise offered this final call to action for those considering their own path forward:

“Apply for the ICAN Learn scholarship to become qualified, represent our mob, and be part of real change in the sector. The benefits go beyond the classroom, it brings job stability, career growth, and personal empowerment. I feel so enlightened now, and I’m proud to be qualified to give real advice… even if my son cringes at it sometimes!”

Applications for the 2025 ICAN Learn Scholarships are now open. Apply for yours today!

ICAN Learn can also help with your corporate training needs. To find out more, contact us at administration@icanlearn.edu.auor phone (03) 5471 7777.

ICAN Launches the ID and Banking in Prison Project

ICAN is proud to announce the launch of the ID and Banking in Prison Project, an innovative initiative aimed at addressing one of the most significant barriers to reintegration for men in custody at Lotus Glen Correctional Centre (LGCC): access to proper identification. Funded through the ICAN Grow Fund, this project will provide essential Transport and Main Roads (TMR) Adult Photo IDs to approximately 700 vulnerable men over two years, supporting their financial and social inclusion both during custody and after release.

Why Identification Matters

For many vulnerable individuals, including those in custody, a lack of identification prevents access to vital services like banking, housing, healthcare, education, and employment. This challenge is particularly pronounced for First Nations peoples and those from remote and regional communities.

The consequences are far-reaching: without proper ID, individuals face financial exclusion, difficulty accessing social benefits, and barriers to securing stable housing or employment. These obstacles increase the likelihood of reoffending, perpetuating cycles of disadvantage.

Research, including the New Zealand report Paying the Price, underscores those equipping prisoners with proper ID and facilitating access to banking services before release is critical to reintegration and reducing recidivism. This project addresses these challenges head-on.

Tackling the Problem at LGCC

At LGCC, ICAN’s outreach team identified the urgent need for identification. A comprehensive audit revealed that:

70% of respondents required a photo ID.

19% were without a bank account or had lost access to one.

83% of men entering custody identified as First Nations, many from remote communities where access to services is limited.

These findings informed the design of the ID and Banking in Prison Project, which aims to eliminate barriers to obtaining identification and accessing essential financial services.

A Streamlined Process

In partnership with Queensland Corrective Services (QCS) and Lives Lived Well – CREST Re-entry Services, ICAN will provide financial support to cover TMR Adult Photo ID application fees. The project leverages a Memorandum of Understanding (MOU) between QCS and TMR, allowing QCS-issued ID to meet application requirements, bypassing the need for secondary documents like birth certificates or utility bills.

Key components of the project include:

Screening and identifying prisoners in need of photo ID.

Assisting with application completion, and addressing literacy barriers.

Funding application fees to ensure access for those unable to afford it.

Facilitating banking access using the newly issued TMR ID.

Delivering Meaningful Change

This project is expected to create a lasting impact by:

Providing 700 men with TMR-issued Adult Photo IDs.

Reducing barriers to accessing banking, housing, and other essential services.

Enhancing collaboration among ICAN, QCS, and CREST to maximize resources.

Informing long-term solutions to identification challenges through an independent Impact Report.

Building a Brighter Future

Through this initiative, ICAN is taking a critical step toward addressing the structural barriers that perpetuate disadvantage among vulnerable populations. By supporting access to primary identification and financial services, the ID and Banking in Prison Project aims to empower men in custody to reintegrate successfully and reduce the risk of reoffending.

This transformative project is made possible through the ICAN Grow Fund, which ensures that 100% of every donation is sustainably invested to create real, measurable change. By contributing to the fund, supporters are directly enabling initiatives like the ID and Banking in Prison Project, empowering individuals to build a brighter, more inclusive future. Donate to the ICAN Grow fund and follow the impact of your investment today.

FCAQ recently released its report ‘Give Financial Counselling in Queensland a Fair Go’ requesting $15M per annum from the Queensland Government over five years to support state-based financial counselling services. With the burgeoning demand for services and the cost-of-living crisis, we asked ICAN’s Operations Manager, Jillian Williams, how the sector is coping when there’s just no letting up.

Great to yarn with you again Jill!

First up, with an unprecedented surge in demand for financial counselling services across Australia, how is the sector coping?

Financial counsellors are incredibly resilient professionals who, despite surging demand for their services, can maintain their commitment to and focus on the needs of the people seeking their help. The concern for financial counsellors when demand surges is how we can help as many people as possible through these really tough times. Despite that passion and resilience, the fact that there are too few financial counsellors to assist the many people who need our help impacts the wellbeing of the people in our sector. As community service providers, we live and work alongside the people who need us. We see the pain and know that financial counselling can ease the significant stress that so many people are living with. It inevitably takes a toll on us when we can’t get to those people.

Financial counsellors are facing an overwhelming demand for services. How does chronic demand impact their wellbeing and morale?

Financial counselling services manage demand differently depending on the communities in which they work. ICAN has always had a waitlist of clients seeking our help. As this wait list has grown over the past 4 years, it has come to represent the significant gap between demand for our service and the number of financial counsellors available to assist. Our team view the waitlist regularly as part of our triage services; it is an ever-present reminder that we can’t get to everyone we need to. Knowing that people are having to wait too long to get to us inevitably impacts morale and wellbeing. When care and passion for the work you do to support people collides with the stress of not being able to help enough people, burnout occurs. This can have a knock-on effect across teams, and overall morale and wellbeing take a hit. We constantly manage the pressure to support more people than we can realistically assist at any given time.

What is the largest barrier to people in financial hardship accessing financial counselling?

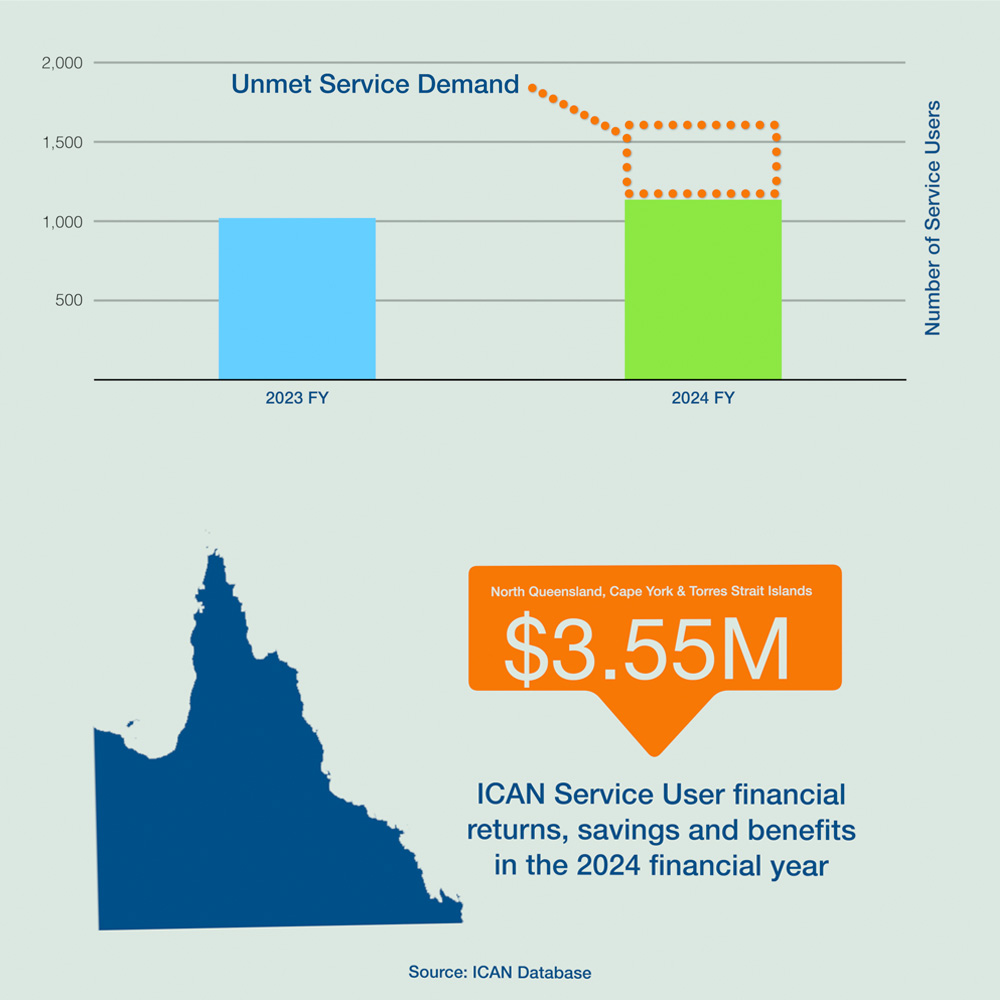

Currently, the biggest barrier is that there are simply not enough financial counsellors to meet the demand for this vital service. We have a waitlist of over 6 weeks across all of our offices and have had to turn new clients away many times because we simply did not have enough financial counsellors to see the many people contacting us for the first time to get help.

The other challenge is that many people have no access to face-to-face financial counselling, particularly in regional and remote communities, who desperately need these services. Travel to these communities is not funded, and the significant hurdles people face with poor digital connectivity and low digital literacy means that phone and internet services are not always effective. People can experience overwhelming shame in talking about finances. Face-to-face contact is often necessary to build trust in the financial counsellor so that a person feels safe enough to open up about their money worries.

Do organisations face any risks due to ongoing chronic service demand?

Organisations can lose some of their best people when staff are burning out due to overwhelming demand. In and of itself, this is a terrible outcome. We don’t want peoples’ wellbeing impacted through the work they do. At an organisational level, it means we have to recruit and train new people in the role, which can have a flow-on effect with experienced staff needing to work harder to support the development of trainees while also managing more complex client casework. This training period is important – we want new people entering the sector! However, there has to be funding to support their development to take on more complex casework. There are no easy solutions to these workforce issues, particularly if there is insufficient funding to support professional development and the costs of structural changes often needed to support teams.

How do people under financial stress respond when advised they must be waitlisted or referred elsewhere?

In all honesty, it depends on the person. Most people are understanding and quietly accept our wait times – this doesn’t mean they aren’t hurting; it just means they don’t like to complain. Then, there are those our reception team engages with daily who express their understandable stress and frustration about waiting. Their reactions are in response to the reality that they are in so much debt they can’t put food on the table for their kids, or their sole means of transport – the family car – is at real risk of being repossessed, or their rent is so far behind they are facing eviction. Whatever peoples’ reactions to their situation and the challenges in engaging with services, we know everyone is doing the best they can in really difficult situations.

In all of this, receptionists are the unsung heroes of the community sector. They are skilled in tackling really challenging and often very emotional conversations with people in the community who are hurting. They are the first interaction that people will have with a service and can be the difference between a person feeling confident and safe enough to pick up the phone and engage with the service again.

FCAQ’s survey revealed Queensland Financial Counsellors want funding for more specialist training in gambling, domestic violence, prison work, and small business. What are the benefits of investing in this training?

The benefit of investing in this training is that we build a financial counselling sector that can work with people across the community who have complex needs. Fewer people are turned away because the service doesn’t feel they have the skillset to assist.

Working with someone who has a gambling addiction (or any form of addiction) or someone who has experienced domestic violence requires specialised knowledge of how these experiences are impacting their finances and their wellbeing. For example, addictions, whether gambling or otherwise, impact peoples’ money story and working with them to resolve their money issues can be challenging if they are not ready to admit to the addiction or address it. For people experiencing domestic violence, their safety is paramount and ensuring our work does not threaten this is critical and not always straightforward. For instance, getting a joint debt waived that results in the perpetrator being forced to pay immediately puts the victim/survivor at risk of violence. We have to work to minimise this risk while also ensuring the victim/survivor is not carrying the financial burden of the perpetrator’s debts. Working with people in prison fundamentally involves a different way of working. There are barriers to engaging with financial services that people outside prison don’t experience, and financial counsellors have to find workarounds that aren’t required in usual service delivery.

And then there are specialist areas of work that require an understanding of different laws and systems but equally involve working with people experiencing significant stress, such as small business operators who have lost their business.

For all of these people, it is necessary to understand the impact of any trauma they may have experienced or are experiencing through their individual situation. These are all complex skills requiring an understanding of addiction; mental health; and the criminal justice and financial services systems.

The BOM predicts a scorching summer for Australia and potentially severe weather nationwide. With financial counselling services already stretched, how can the sector cope with climate change disasters without the necessary funding?

The blunt reality is that we can’t. Current funding is not meeting the demand in the communities that have not been impacted by climate disasters. When a disaster strikes, as it did for us in Cairns following cyclone Jasper, there is no additional resourcing that can be employed to reach the people affected. Services are stretched too thin on the ground as it is. And often, even where funding is provided, it is not as simple as recruiting more financial counsellors. There just aren’t enough qualified financial counsellors in regional areas, so investment in training and developing new financial counsellors in regional areas is critical so that we have qualified people available to respond when a disaster strikes.

As the demand for financial counselling services grows, what developments do you think will shape the sector’s future?

As the sector gains much-needed support from industry funding in the coming years, it will be important for us to hold the activism that has been at the heart of this sector from its inception at the forefront of our minds. Demand is growing in large part because there continues to be poor responses by industry to the hardship people face, and exploitation of people’s hardship inevitably occurs in some pockets of industry. As we enter this new funding landscape, we must be confident as a sector in calling these industry failings out and not be fearful of taking strategic action when our concerns are not heard.

In addition, increasing demand for financial counselling services will require our sector to adapt and trial different ways of providing our services. Intake, referral and service delivery processes may change as services seek better, more efficient ways to meet demand. Other community services will be similarly adapting, which opens up real opportunities to create a more networked and integrated community service sector that can respond holistically to the needs of the community.

However, there is a risk that community services increasingly relying more on centralised, digital platforms to deliver services, just as government and private industry already have. While these platforms may work well for many people, they pose significant barriers for those in the community who experience digital exclusion and other vulnerabilities. These are people who will always need to have direct contact with the person with whom they have to share their story and their fears in order for them to move from surviving to thriving. These are the interactions that give our sector its heart. As services adapt and innovate, this reality can never be forgotten, because removing that contact for the sake of simply ‘helping’ more people faster will not meet the underlying needs of the people seeking our services.

Remember Elise Deemal who was living the dream as a Yarnin’ Money Mentor last time we yarned? Thanks to CBA’s First Nations Scholarship Program she’s now on track to graduate as a Financial Counsellor later this year and thriving in her new role with ICAN’s Prison Project. We caught up with Elise to get the scoop on her amazing journey.

Hi Elise, it’s great to yarn again!

When we caught up in September 2023 you were working as an ICAN Yarnin’ Money Mentor while completing the CHC51122 Diploma of Financial Counselling Fast Track through CBA’s First Nations Scholarship Program. Can you tell us what you’ve been up to since then?

Hi guys, thanks for having me back 😊. Well let me tell you I have been busy to say the least, transitioning from my role as Yarnin’ Money Mentor to Financial Counselling Support Officer Trainee, my study, and family time. But I’m loving every minute of it.

Can you tell us what receiving the Fast Track Scholarship means to you?

Receiving the Scholarship not only provides me with the opportunity for higher learning, it’s given me the opportunity to build my future and to be a role model for my family and my people. Not a lot of us in my family had the opportunity for higher education, we just go out into the workforce to earn money for our living, as opposed to working in something that you’re passionate about, and I’m really passionate about financial counselling.

What’s your study experience with ICAN Learn been like?

It’s fantastic – and challenging at times! Not only am I’m gaining the knowledge to become a professional financial counsellor, but I’m learning how to work within frameworks, and how to conduct myself ethically both in my professional and personal life. It’s also taught me to be much more organised so I can balance work, study, and family. It’s really brought a new awareness into my life and is changing the way I view things.

I also really enjoy learning online – for me it makes the learning more personal. The ICAN Learn trainers are amazing, especially their acknowledgment of country and First Nations people. It’s a great career path for First Nations peoples, we desperately need more in the sector.

Why did you choose a career in Financial Counselling?

After I accessed my own financial counselling in my twenties and I knew that it was what I wanted to do. Back then I was a full-time working mum hustling for my family, with no time to study. Now it’s my turn. Starting out as Financial Capability Trainee was a foot in the door to a career in financial counselling. I’m at a place in my life where I feel like I can take control of my future.

You’re now part of ICAN’s Prison Project Financial Counselling team, can you tell us more about that?

It’s been an exciting time for me. Coming from a legal services background made the transition smooth. My colleagues in the Prison Project team are awesome, and the clients I assist make it easy to come to work every day. My manager, Sharon Edwards, is an incredible person. She is passionate, patient, and has a great wealth of knowledge. It really shows in her work and the way she helps our clients, she really listens to every word. I feel incredibly grateful to be learning from her.

What sort of issues surprised you when you started providing services to inmates?

What’s surprised me most is the level of need and the types of issues, such as ID and banking challenges, it makes life very difficult. Money is part everyday life, even in prison. People who are incarcerated cannot self-advocate. They’re not allowed to call their financial institutions. They have time limits on their phone. So to have ICAN visit the centre is a relief for inmates. Being able to help someone manage or set up a bank account while they’re inside is one less worry for them to deal with and helps them reintegrate into society more easily on release. I always feel safe when I’m in and around the centre, and the staff are great. Not everyone can do this work, but I think there needs to be an understanding that inmates also have rights. For me, it’s not about their offending, it’s about their financial life.

Why is it important to have more First Nations peoples working in the Financial Counselling sector?

There’s not a lot of familiar faces in this profession, so I think it’s important that First Nations people are in these sorts of roles to empower our people, our communities, and to let them know that they can do this work as well. As a First Nations person, wherever I go in Australia – or in my profession – I feel like I’m in the minority. Whereas when I visit the prison, I am in the majority. It’s a good change for First Nations inmates to have a familiar face helping them with their financial hardship, and they feel more comfortable sharing their story with me.

ICAN provides financial counselling to Indigenous and non-Indigenous people. As a First Nations woman, I believe everyone had the right to achieve financial wellbeing. Seeing our non-Indigenous clients embrace my help is very important to me, it means a lot.

What would you say to encourage other First Nations people to apply for a Scholarship with ICAN Learn?

I would say that Financial Counselling is a wonderful sector to be a part of, I love it so much. It doesn’t matter what age you are when you start studying, you can make a real impact in people’s lives that could change the course of their life.

Financial literacy for modernity is so important. Times are rapidly changing with technology, cyber scams, and the cost of living. The need for financial literacy has never been greater. It’s an important skill for us to have to continue to succeed in today’s world. And the beauty about this learning is that no one can take it away from you.

You can read more about ICAN’s work with prisons here

Or find out more about ICAN Learn Scholarships here

Do you need help with your personal or corporate training needs? Contact ICAN Learn at: E: administration@icanlearn.edu.au T: 03 5471 7777

ICAN is leading the charge in addressing changes to banking systems for people in prison. In a recent submission to the Australian Bankers Association (ABA) Code of Banking Practice Review, ICAN highlighted five practical recommendations that the banking industry can make to address current inequities. The recommendations tackle the structural barriers witnessed first-hand by ICAN financial counsellors, Sharon Edwards and Alex Price-Busch, in their fortnightly outreach service to Lotus Glen Correctional Centre (LGCC).

“People entering prison, often come with debts which they have limited information about,” said Sharon. “Their ability to obtain information to deal with the debts is near impossible, due to the many barriers faced inside. Unresolved debts grow through additional fees and interest charges while in prison, resulting in an unmanageable debt upon release.”

A 2019 Queensland Productivity Commission Inquiry (p359), reported on the link between unresolved financial issues and stress for people inside prison, and the compounded risk of reoffending because of increased indebtedness. ICAN Operations Manager, Jillian Williams highlights banks, and the products and services they provide are critical tools for managing the essential needs of day-to-day life.

“Banking products and services remain crucial for people incarcerated,” said Jillian. “We are trying to amend systems that will allow people in prison to keep managing their financial lives while on the inside. What we really need from the banks is for them to acknowledge that people in prison, and those transitioning out, experience vulnerable circumstances and amend the Code of Banking Practice accordingly.”

In a growing movement for change, Financial Counselling Australia, and the Thriving Communities Partnership, have championed the impact of financial issues on people in prison in their reports; Double Punishment: How people in prison pay twice and Fostering Financial Stability for People in Prison Project. As highlighted in these reports, people entering prison will come with many and varied debts which they have limited information about, and which will often go unaddressed or unresolved.

Through a partnership with LGCC, in Far North Queensland, ICAN Trainer, Majella Anderson and Financial Counsellor, Alex Price-Busch deliver our financial capability program, Yarnin’ Money, once a month. The participant stories and comments shared in group training or one-on-one financial counselling sessions, best characterise the need for systems change:

“It is such a relief to know you can help. I had no way of letting them know I was here. I was worried I could lose my house.”

“My bills and things have been stressing me out so much, I couldn’t sleep.”

“I worry about my family on the outside. If I can’t deal with my bills and things, it will only make it worse for them.”

“I really want to straighten everything out while I’m here so I can have a fresh start. I want to be able to rent a place for me and my son and buy a car. If I had a car, I could take my son to footy and I could get out of the ‘Bronx.’”

Lotus Glen Correctional Centre and ICAN partnership participants.

Lotus Glen Correctional Centre (LGCC) has partnered with the Indigenous Consumer Assistance Network (ICAN) to focus on delivering strong financial skills training for prisoners.

The focus of the collaboration is to increase prisoners access to skills such as budgeting and management of finances which are critical skills for everyday living.

These skills bring a value of self-belief and a positive affirmation for the prisoners and the struggle of debt and lack of financial understanding within the prisoner cohort causes stress, angst and a loss of self-confidence.

Service Delivery Support Officer (SDSO) Tania Parker and Indigenous Consumer Assistance Network (ICAN) Financial Counsellor Sharon Edwards got together to look at how a partnership could address these concerns, and assist in providing an opportunity of change for the prisoners by providing tools for the prisoner to feel confident in the management of their personal finances upon transition back into the community.

ICAN CEO, Aaron Davis said the collaboration with LGCC was an opportunity to help prisoners regain financial control of their lives and teach lifelong skills to help them support themselves.

“We are really excited about this opportunity to empower people that have often had very complex and dynamic lives, “ Mr David said.

“We know that debts don’t magically disappear when someone goes to prison and can become one of the greatest barriers to re-integration and rehabilitation.”

“For ICAN, our focus is on breaking down this barrier by providing financial counselling support to manage existing debts and education to promote good financial literacy in their future.”

With the assistance of the SPER Hardship Partners Team from Queensland Treasury, a strong partnership has been formed.

Twenty men have successfully completed their first Yarnin Money workshop, with eighteen continuing on with individual one-on-one financial counselling.

Due to the success of the program, Yarnin Money has now become a LGCC staple program, and ICAN a part of the LGCC community.

Above: Tania Parker and Sharon Edwards

Tania Parker SDSO said the response from prisoners about the program had been very positive.

“Our goal is to provide this fantastic opportunity to as many of our prisoner cohort as possible, and we have received very positive feedback about the program,” Ms Parker said.

“All the participants were engaged, they shared ideas and stories, and have spoken to other prisoners about their positive experience within the program, which has generated great interest amongst the prisoners.”

ICAN Financial Counsellor, Sharon Edwards said that interest and uptake of the service has been overwhelming and this is an area of great need.

“There are numerous impediments to the provision of financial counselling in a prison setting, like meeting creditor identification requirements, providing evidence of low income, to just general day-to-day client contact.” Ms Edwards said.

“By working together to identify and remove some of these barriers for prisoners, our partnership has also streamlined access to the Work Development Order Program.”

“Participants now have the ability to reduce their SPER debt through accessing our service in the prison. I believe this is a first for Queensland.”

SPER’s Hardship Partner program gives people in genuine hardship realistic options to resolve their debt. Delivering this program with partner organisations like ICAN has been key to ensuring debtors experiencing hardship have access to such options, including Work and Development Orders. Partnerships like that which Sharon and Tania have established between ICAN and LGCC means prisoners have access to this program and can now work towards getting on top of their debts.

Make a Donation to the ICAN Grow Fund by using the Paypal donate button below.

ICAN Launches Grow Fund

ICAN is proud to announce the launch of the ICAN Grow Fund, a transformative initiative designed to address financial barriers and create pathways for empowerment and inclusion for First Nations peoples. “The fund will enable ICAN to invest in groundbreaking projects, develop innovative programs, and expand partnerships that foster sustainable economic growth,” said ICAN CEO, Aaron Davis.

The ICAN Grow Fund

The ICAN Grow Fund is fueled entirely by donations, with 100% of contributions sustainably invested to create real, measurable change. The fund focuses on:

Research: Uncovering and addressing financial barriers faced by First Nations People.

Program Development: Crafting innovative solutions that meet community needs.

Capacity Building: Strengthening governance and leadership for impactful work.

Partnership Expansion: Driving collaboration for sustainable growth.

“The fund provides a direct avenue for supporters to contribute to initiatives that empower First Nations people to take control of their financial futures,” Mr Davis explained.

The First Initiative: ID and Banking in Prison Project

The ICAN Grow Fund’s inaugural project, the ID and Banking in Prison Project, addresses the critical need for identification to support financial and social inclusion among vulnerable men in custody at Lotus Glen Correctional Centre (LGCC) in Far North Queensland.

In partnership with Queensland Corrective Services (QCS) and Lives Lived Well – CREST Re-entry Services, ICAN will fund approximately 700 Adult Photo ID applications over two years. This project aims to reduce barriers to essential services such as banking, housing, healthcare, and employment by providing primary identification to First Nations men in custody.

Why Identification Matters

A lack of proper identification often prevents individuals from accessing vital services, exacerbating financial and social exclusion. This issue disproportionately affects vulnerable populations, including those in custody. Research will highlight those equipping prisoners with necessary identification and facilitating access to banking services is critical for successful reintegration and reducing recidivism.

Highlighting the urgency of the project, ICAN prison Project Manager, Sharon Edwards said, “ICAN partnered with LGCC Programs staff to undertake a comprehensive banking and ID audit over three months. The results were telling, with 70% of respondents stating that they needed a photo ID, and 19% stating that they didn’t have a bank account or had lost access to one.”

“Eighty-three percent (83%) of men coming into the prison identified as First Nations,” said Ms Edwards. “Many of these men originated from regional and remote communities across Far North Queensland, where access to banking and transport (TMR – ID) services are limited.”

Project Methodology

The project involves a streamlined process that leverages a Memorandum of Understanding between QCS and TMR, allowing QCS-issued ID to support applications. CREST and ICAN staff will assist prisoners with the application process, addressing literacy barriers and financial constraints.

This initiative will:

Provide 700 vulnerable men with TMR-issued Adult Photo IDs.

Enable access to essential banking and financial services.

Collect quantitative and qualitative data to inform future initiatives.

Expected Impact

ICAN will engage Dr Heron Loban to produce an independent Impact Report that will demonstrate the project’s success and identify opportunities for scaling. Deliverables include:

Enhanced financial and social inclusion for men in custody.

Reduced barriers to reintegration post-release.

Increased collaboration among ICAN, QCS, and CREST for long-term solutions.

Join the Movement

The ICAN Grow Fund is a bold step toward creating lasting change. By investing in projects like the ID and Banking in Prison Project, we can help break down barriers, empower individuals, and drive sustainable economic growth for First Nations People. Please contribute to the ICAN Grow Fund today, together we can grow a brighter future for all.

NAIDOC Trivia Team Winners show off their huge trophies! As Australia marks 50 years of NAIDOC Week, the 2025 theme, The Next Generation: Strength, Vision & Legacy, holds deep significance for the Indigenous Consumer… Read more »

Understanding superannuation just got easier, thanks to a new collaboration between the Indigenous Consumer Assistance Network (ICAN), AustralianSuper, and the First Nations Foundation. Responding to requests from community members, the team produced the Super… Read more »